What a quarter. It’s been a year since the UK first went into lockdown. High street icon Topshop has closed its doors for good. We’re edging towards life post-lockdown (while reminding ourselves it’s data not dates that will get us to that pub garden).

Things look, dare I say it, hopeful. But while the prospect of a family barbecue fills us with joy, things changing yet again is likely filling most retailers with anxiety. Just as you’re getting to grips with how the pandemic has changed consumer shopping behaviour, Boris’s announcement throws everything back up in the air.

After a year of shopping almost entirely online, how will consumers behave once brick-and-mortar stores reopen for good? Should brands continue to prioritise online channels, or should they reallocate budget to the in-store experience? Will pureplay online businesses see sales slump after a year of record growth?

To find out, we’ve analysed data from more than 450 brands across sectors. Here’s how consumers shopped in Q1 2021 – and how we predict they’ll shop in Q2 and beyond.

Side note: To keep things simple, our graphs show activity from the start of lockdown on 23rd March 2020 to the same date this year.

Consumer buying behaviour in 2020: a recap

Despite headlines warning of mounting debts and a looming recession, 62% of consumers feel financially better off or the same as before Covid. For those fortunate enough to have stayed in work at full pay, the lockdown has been an opportunity to save. Instead of eating out or going on holiday, consumers have treated themselves to online shopping.

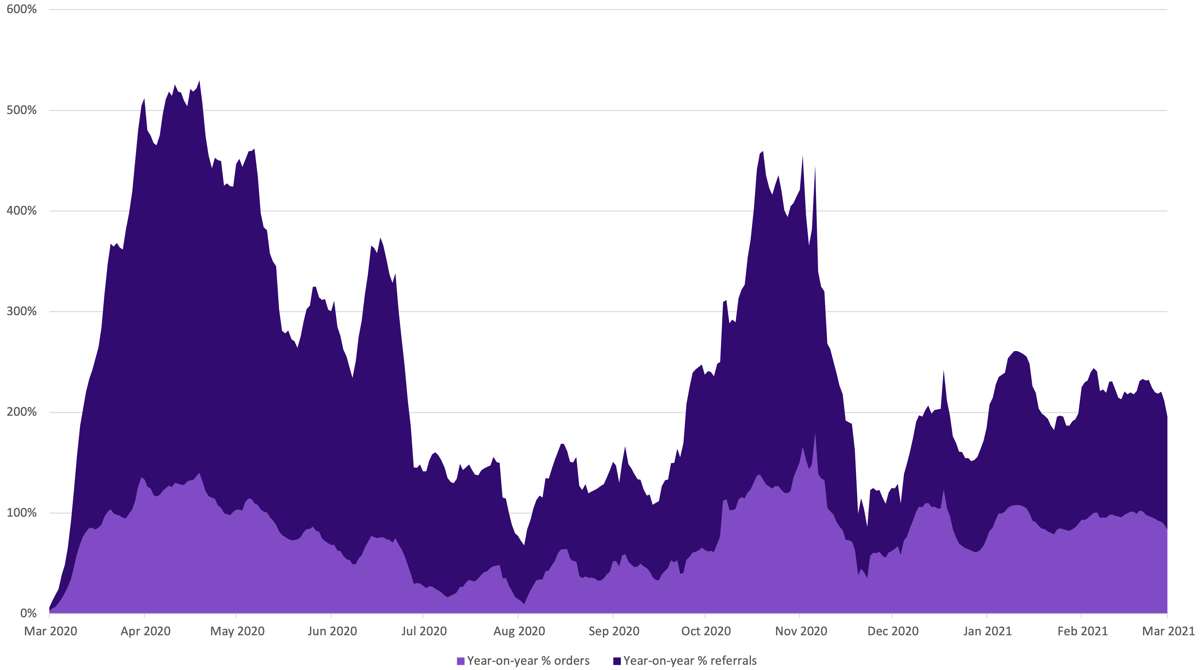

According to online retail body IMRG, online sales grew by 36% in 2020 – the highest growth rate in 13 years. As well as buying from their favourite online brands, consumers recommended them to friends and family. In 2020, referrals across the five most popular sectors* peaked at 420%.

* That’s home and garden, food and drink, fashion, beauty and gifts.

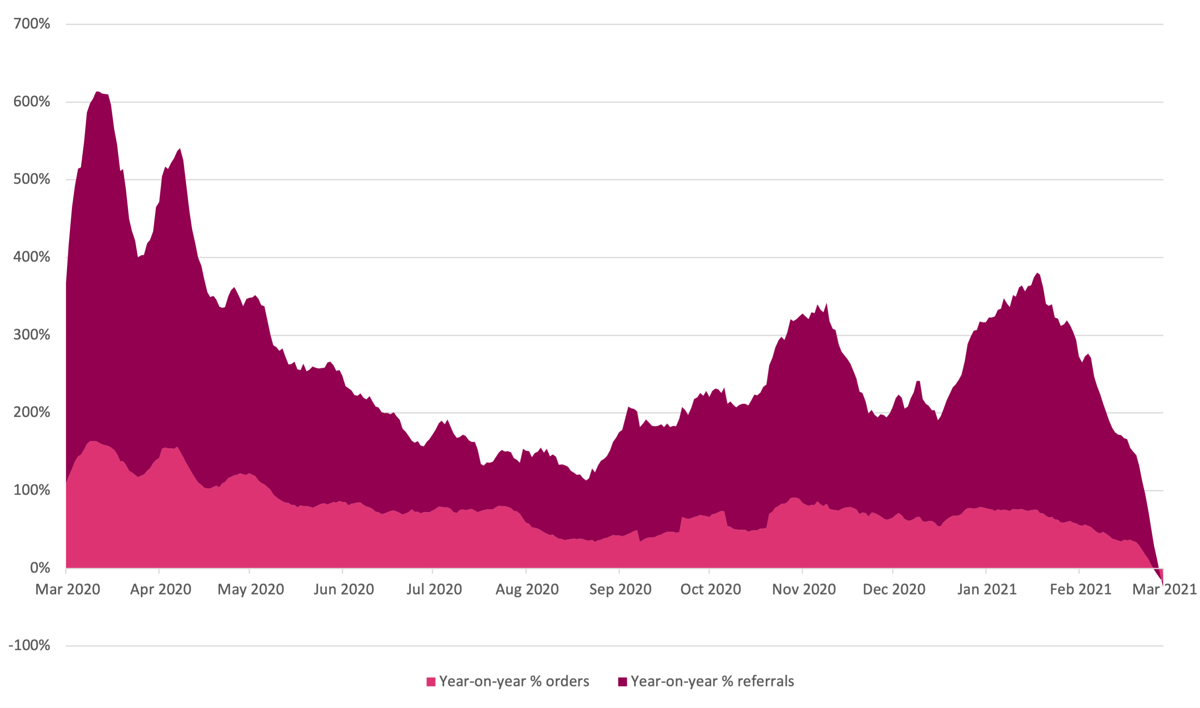

Food and drink

When lockdown 1.0 began on 23rd March 2020, food and drink brands were the first to see online orders soar. Panicked by empty supermarket aisles and rumours of broken supply chains, people quickly discovered – and told their friends about – online brands that could keep their kitchen cupboards stocked.

Fast forward to January this year, and consumers were still recommending their favourite food and drink brands. Online orders for our clients in this sector peaked at +79% YoY in mid-January. By early February, referrals were up 307% YoY.

Now consumers are no longer worried about going hungry, online orders and referrals are unlikely to match last year’s levels. Nonetheless, we expect both to stay strong this quarter.

The pandemic meant more people discovered online brands that could help them eat better, from vegan ready meals to easy-to-follow recipes. While outdoor hospitality venues reopening from 12th April may cause sales of restaurant-style mealkits to decline, consumers are likely to continue recommending brands offering more everyday products, such as veg boxes and speciality mealkits. We anticipate volumes in this sector reaching similar levels to Q3 last year, when orders were up 50% YoY and referrals hovered around +70% YoY.

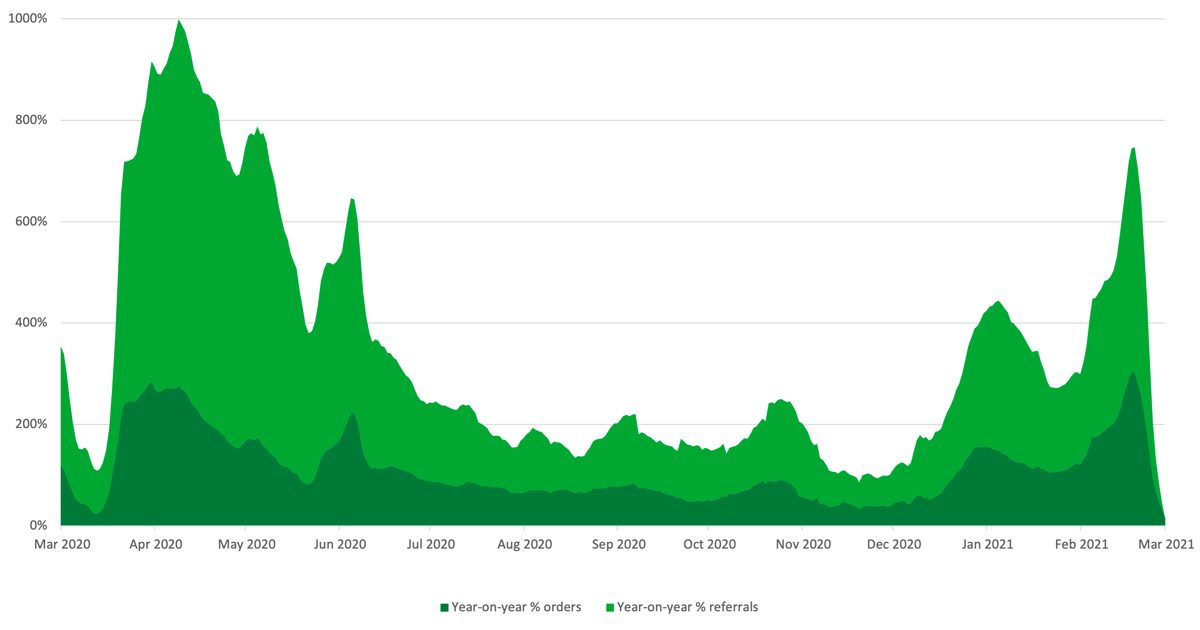

Gifts and occasions

The gifts and occasions sector has thrived in lockdown. Without the option to browse in-store, consumers have gone online to treat their nearest and dearest. The desire to support one another over the past year has further boosted online gift sales, with many consumers sending gifts ‘just because’, rather than for specific occasions.

Q1 counted two calendar events this year: Valentine’s Day and Mother’s Day. The changing date of Mother’s Day each year partly explains the significant peak two days before, with referrals +444% YoY on 13th March – the biggest uplift of all the sectors. Online orders on the same day reached +303% YoY.

The pandemic has opened consumers’ eyes to the vast array of gifts available online, from personalised biscuits to fresh flowers and bespoke stationery. Delivery is an added bonus, removing the need to travel unnecessarily and put those waiting for vaccines at risk. Despite non-essential shops reopening from 12th April, we anticipate orders and referrals for brands in this sector remaining twice as high as pre-pandemic.

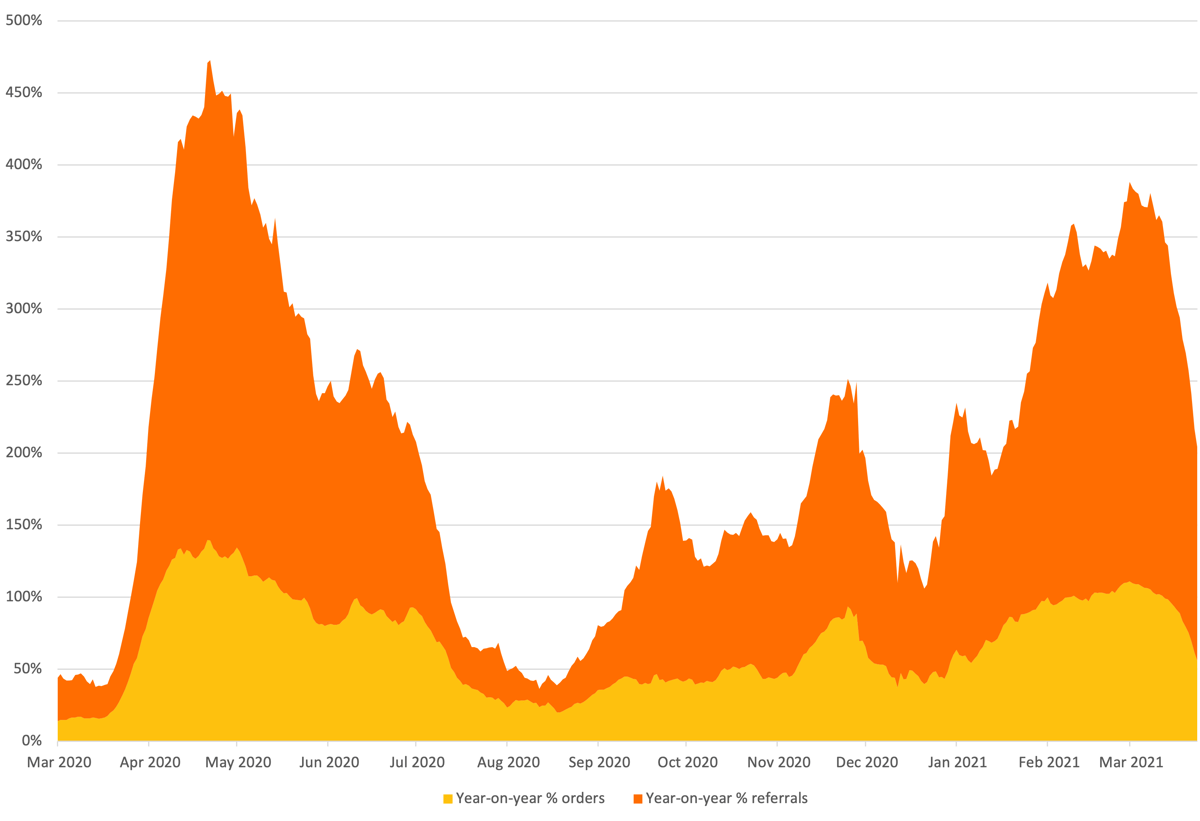

Home and garden

Online orders and referrals for our home and garden clients held consistently strong this quarter. After a dip in early January, referrals picked up pace, reaching +258% YoY in early February.

Then, on 22nd February, Boris Johnson announced the roadmap for exiting lockdown.

In the week that followed, referrals rocketed. By early March, they stood at +277% (online orders were at +111%). As consumers prepared to welcome other households to their gardens from 12th April, they snapped up items like barbecues and garden furniture.

While most homes have now adapted to lockdown, we expect online brands in this sector to remain in demand. Products like ergonomic desk chairs may no longer be on the shopping list, but accessories such as houseplants and wall prints remain hot topics of conversation thanks to never-ending Zoom calls. The stamp duty extension has also spurred more people on to buy their first home and seek recommendations of where to buy furniture and other big ticket items. And with summer fast approaching, garden plants and outdoor equipment are set to be high on shopping lists, especially with holidays abroad off the cards.

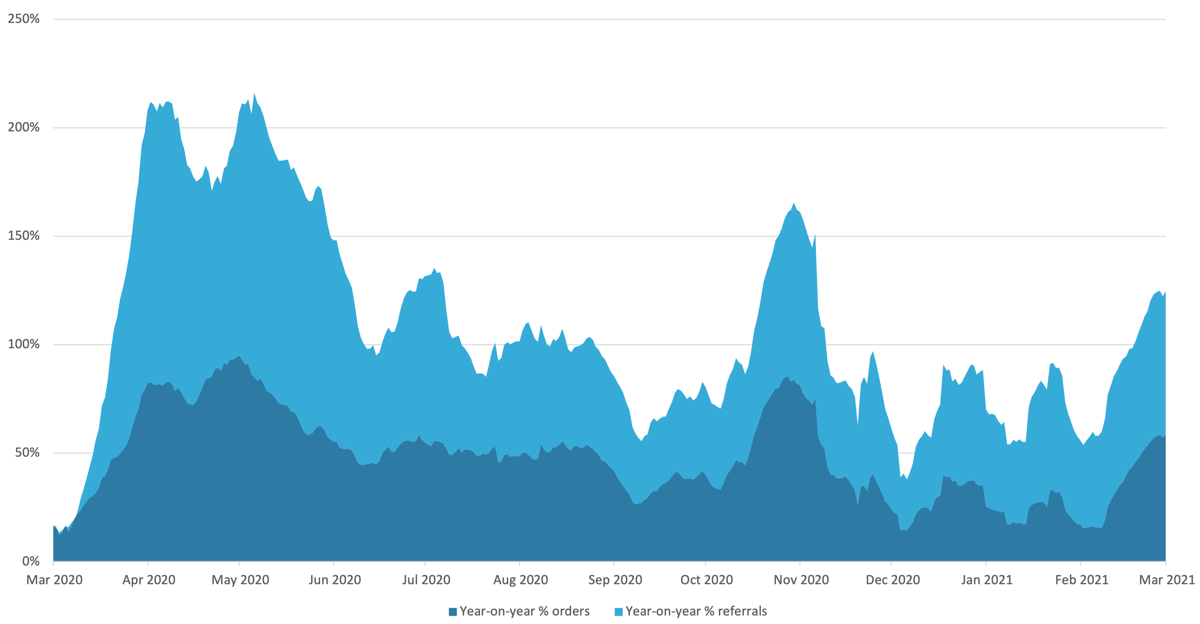

Fashion

Online orders and referrals for fashion brands have been steadily rising since early February. By the end of Q1, they were up 58% and 66% respectively. After a turbulent 2020, things are looking positive for this sector, with even online footwear sales up for the first time since 2019.

Right now, fashion is the only industry with online orders and referrals on an upwards trajectory YoY. As people prepare to abandon loungewear for good, they’re asking their friends for recommendations of where to shop. And with social events like weddings finally back in the diary, they’re more willing to splash out on outfits that will make them look and feel good post-lockdown. We predict fashion referrals to continue increasing throughout Q2.

Beauty

Beauty brands have been one of the surprise successes of the past year. It seems that when stuck at home, consumers don’t stop buying beauty products – they just buy different ones. Rather than splash out on contouring kits and eyeshadow palettes, consumers invested in skincare in Q1. The stress of the past year has been enough to make anyone’s skin flare up, and when better to finally master that nine-step skincare routine than in a national lockdown?

Though consumers will likely switch up their beauty buys leaving lockdown, we expect referrals and online orders in this sector to remain 50% higher than in Q2 2019. At present, online orders and referrals are up 83% and 111% YoY respectively.

How will consumers shop in Q2 2021?

When referrals and online orders began rocketing for our clients back in March 2020, we were cautious. As the pandemic stretched on, would consumers tire of buying from and telling friends about their favourite online brands?

One year on, it’s clear the answer is no.

In Q1 2021, online orders and referrals across our five most popular sectors peaked at 130% and 245% respectively. Regardless of easing lockdown regulations favouring some industries more than others, we expect these figures to remain high throughout Q2.

Covid-19 has changed consumer lifestyles. It’s opened our eyes to how we can better spend our time, instead of wasting it on long commutes or fruitless shopping trips. Now we’ve discovered the benefits of doing more from home, there’s no going back.

While much of 2021 remain uncertain, all signs point to the pandemic permanently changing shopping habits. When non-essential stores temporarily reopened in summer 2020, online orders remained up 54% year-on-year across our five biggest sectors. Retailers including Topshop and John Lewis have closed physical stores (16 in the case of the latter). 90% of those aged 55+ now shop online.

Nobody knows for sure how consumers will shop this year, including consumers themselves. But we do know two things for sure.

One, brands without an online offering won’t survive. Legacy retailers that once ruled the high street must now act like digital challenger brands to keep market share. Meanwhile, pureplay online brands must keep innovating to stay ahead of consumer behaviour and compete with the hefty marketing budgets of multichannel retailers.

Two, brands that get people talking – for the right reasons – will thrive. Referred customers typically spend 25% on their first order, have 2x lifetime value, and are 5x more likely to refer others. Create online experiences your customers love enough to tell others about, and you’re set to exponentially grow your business, in the pandemic and beyond.

To connect shifts in consumer behaviour with measurable referral performance, a referral marketing platform helps you track who refers whom and how that impacts acquisition and retention.

What Is a Referral Link? How to Create & Track One

What is a referral link, and how does it work? Learn how to create, share, and track referral links so you can attribute customer-led growth and optimise your referral programme.

.png)

.png)

.png)