Bank Referral Programmes in 2026: Incentives, UX and Differentiation That Drive Qualified Sign-Ups

By Courtney Wylie — February 25, 2026

This guide is for banking, fintech, and growth and CRM teams looking to make referral programmes actually work in a sector where trust, risk, and compliance rules make “just copy what everyone else does” a recipe for mediocrity.

A bank referral programme is a structured way for your existing customers to recommend your services to friends, family, or colleagues, usually with an incentive. Sounds straightforward, but in financial services it’s anything but: unlike retail, usage is often infrequent, products are complex, and customers are naturally cautious about sharing financial details.

In this guide, we’ll show you how to differentiate your programme, choose incentives that actually motivate sharing, reduce friction at every stage, hit the right timing in the customer journey, and track the KPIs that prove your referral channel is genuinely driving qualified sign-ups.

What is a bank referral programme?

A bank referral programme is a structured system that encourages your existing customers to recommend your products or services to friends, family, or colleagues. The mechanics are simple in principle: a customer (the referrer) shares a unique link or code with someone they know (the friend), the friend takes a qualifying action with the bank, and once that action is verified, the referrer receives a reward.

In practice, “qualification” can vary depending on the product and regulatory requirements. For example:

Current or savings accounts: The friend must open an account and make a first deposit or maintain a minimum balance.

Credit or debit cards: The friend may need to complete their first spend on the card.

Loans or mortgages: The referral only counts once the friend’s application is approved and funds are disbursed.

These qualification steps are crucial: they protect the bank from abuse, ensure compliance, and guarantee that rewards are tied to meaningful, revenue-generating actions rather than just clicks or sign-ups.

Why bank referral programmes work (even in a saturated market)

Even in a market crowded with cashback offers, loyalty points, and sign-up bonuses, bank referral programmes still have an edge...because they leverage trust. When a friend or family member recommends a bank, the referrer effectively transfers social proof to the friend, giving them confidence in a high-stakes decision.

Unlike picking a new streaming service or online retailer, choosing a bank involves money, personal data, and risk, so endorsements from people you know carry extra weight.

This trust also translates into higher-quality customers. Referred customers tend to be more engaged, make their first deposit or spend faster, and remain active for longer than those acquired purely through paid channels.

Referrals are a confidence shortcut. They reduce hesitation, speed up decision-making, and increase the likelihood of a meaningful, revenue-generating relationship from day one.

The banking referral landscape (why most programmes blend together)

Referral marketing is now standard across nearly every major financial services provider, making the market feel crowded and fairly uniform. Credit cards, current accounts, and investment platforms all offer incentives to get existing customers to bring in friends—but the structure often looks the same: share a link or code, the friend completes a qualifying action, and both parties receive a reward.

The abundance of programmes has diluted differentiation, making it harder for any single bank to stand out purely on the back of a referral scheme.

Cash bonuses or account credit (e.g., £50–£100 for new account sign-ups)

Investment or fintech incentives (e.g., TransferWise/wise first transfer discount)

Pitfall 1: Indistinguishable incentives

Many bank referral programmes fall into the “cash-for-cash” trap: the referrer receives a standard monetary reward, and the friend might get the same. While straightforward, this approach quickly becomes commoditised.

When every bank is offering £50–£100 for referrals, the incentive no longer differentiates your programme - it just adds to the noise. Customers start to tune out, and referrals become a transactional exercise rather than a meaningful recommendation.

Incentives your bank can test in 2026

Forward-looking banks are experimenting with innovative, differentiated incentives that go beyond simple cash:

Fee waivers – temporarily remove account or card fees for both referrer and friend.

Boosted interest or savings rates – offer higher rates for a limited period to encourage account activation.

Points and loyalty rewards – integrate with existing programmes like Avios, Clubcard, or proprietary schemes.

Partner perks – vouchers or access to experiences with retail, travel, or lifestyle partners.

Segmented logic is key. Mass-market customers may respond best to straightforward cash or points, while premium or high-net-worth clients value experiences, VIP access, or exclusive financial perks. By testing different reward types and targeting them by segment, you can make referrals feel more personal, valuable, and worth sharing.

Most of the examples we looked at reward a referral with cash. In research we’ve done for other sectors like retail, cash was definitely one of the most preferred incentives. However, the problem here is that they are all basically the same reward type and the same value. There is no differentiation value for the consumer.

Best practice: It’s tough to find evidence of any financial services provider breaking the mould. Credit card companies are dancing to their own tune with loyalty points as an incentive but as they all seem to have piled on to that bandwagon the differentiation bonus has dissipated.

Pitfall 2: The social value of sharing is unclear

In financial services, asking a customer to recommend a product can feel risky. Because Unlike suggesting a new restaurant or streaming app, a bank account, credit card, or investment platform carries real money and personal data.

When the social value of sharing isn’t clear, referral programmes struggle to gain traction, even if the reward is attractive. In finance, the perceived risk often outweighs the incentive unless the messaging reframes the act of referring as helpful, clever, or prestigious.

Messaging angles that create social capital in finance

We recommend positioning referrals as a positive, confidence-building action:

“Help a friend win” – frame referrals as giving someone a tangible advantage.

“Smart move” – highlight that sharing is a savvy, informed decision.

“Safer choice” – emphasise trust, security, and reliability.

“Exclusive access” – offer perks that make the friend feel privileged or VIP.

“Limited-time perk” – create urgency while maintaining a sense of value.

Embedding these angles into landing pages, emails, and app prompts, can turn referrals from a transactional task into a socially rewarding behaviour, increasing both uptake and engagement.

Pitfall 3: The process is too cumbersome

Friction kills referrals in any sector—but in banking it hits harder. Financial journeys are already layered with compliance checks, identity verification, eligibility criteria, and lengthy forms. Add a clunky referral flow on top and even your happiest customers will quietly abandon the process.

In regulated environments, customers are particularly sensitive to effort and ambiguity. If they don’t clearly understand what qualifies, when they’ll be rewarded, or what their friend has to do, they simply won’t share. And because banking interactions are often infrequent, you don’t get endless chances to recover that lost intent.

The result? Low participation rates, confused referrers, and customer support teams fielding avoidable queries about missing rewards.

Bank referral UX checklist (7 friction cutters)

If you want your bank referral programme to perform, the experience must feel effortless and transparent. Here’s a practical UX checklist for 2026:

One simple share link: Provide a unique, trackable link. No manual codes, no printable forms, no unnecessary steps.

Minimal input fields: Avoid asking the referrer to input their friend’s details. Let customers share directly via link or native share tools.

In-app referral dashboard: Host referrals inside your mobile app or online banking environment, not just on a static landing page.

Real-time status visibility: Show clear progress: invited → signed up → qualified → reward paid. Visibility builds trust.

Clear eligibility rules (in plain English): State exactly what counts: e.g., “Friend must fund account with £500 within 30 days.” No small-print surprises.

Pre-filled share copy: Provide suggested messaging customers can personalise. Make it easy to sound helpful, not salesy.

Support fallback: Include a clear help link or chat option if something goes wrong. Silence erodes confidence fast in financial services.

The goal is to remove doubt, remove effort, and remove delay. In a regulated industry where complexity is unavoidable, your referral journey should feel refreshingly straightforward.

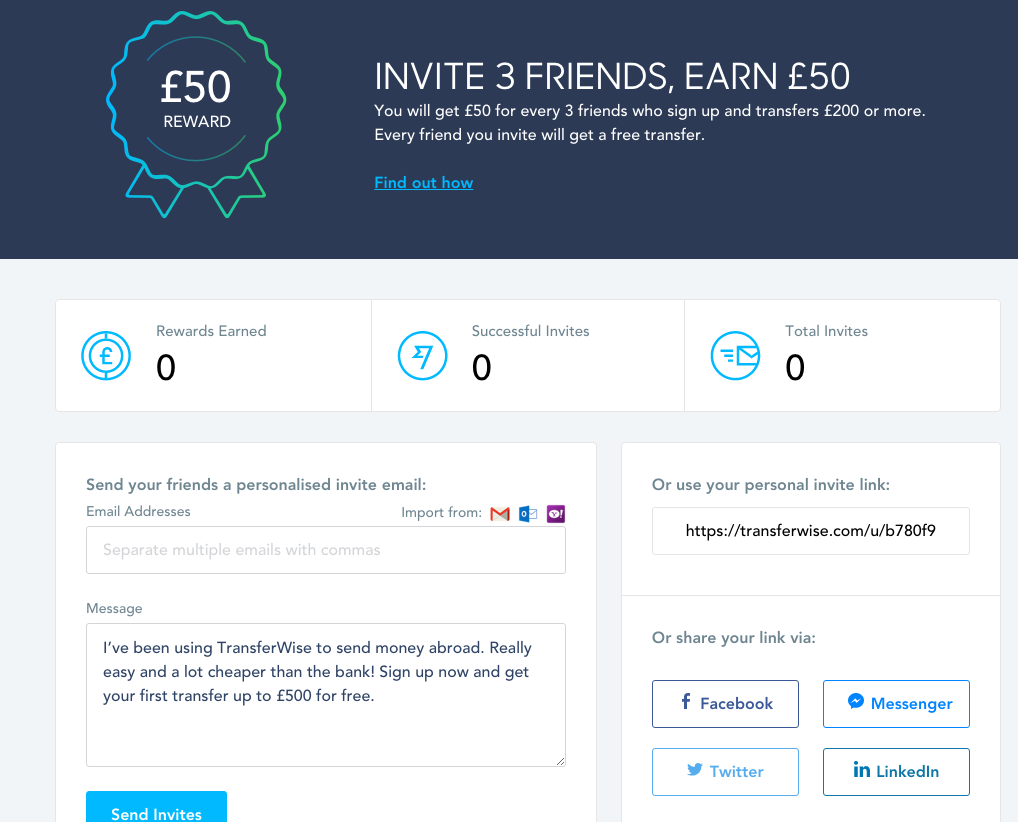

The next level: Take a look at the innovation going on in retail refer-a-friend and copy it, like Transferwise have done. Most outsourced referral platforms now offer customised dashboards like this as a standard part of their service. Here is an example of one which we’ve created recently for a Mention Me client.

Pitfall 4: Too few moments to ask

In many areas of financial services, product usage is infrequent and highly functional. A customer may open a current account and not meaningfully interact with the brand again for weeks. A mortgage customer might not revisit their application journey for years.

That means fewer natural “moments of delight” when enthusiasm is high and willingness to recommend peaks.

If you only promote your referral programme via a static landing page or the occasional email, you're relying on customers to remember it exists. And in banking, where attention is limited and trust is hard won, that's a risky bet.

The solution? Identify and engineer high-intent, high-satisfaction moments and points in the customer journey where confidence is strongest and sharing feels appropriate rather than intrusive.

Best referral triggers by banking product

Different products create different referral triggers, so here are some of the most effective moments to test:

After account funding: Once a customer has successfully deposited money and sees the account live, confidence rises.

After first card spend: The first successful transaction signals activation and usefulness - an ideal sharing cue.

After approval (loan, credit card, mortgage): Approval is an emotional high point. A well-timed referral prompt can convert relief into advocacy.

After first successful transfer (payments or FX): Particularly powerful for international payments, success builds trust quickly.

After first investment deposit: When customers see funds invested and the platform working as promised, sharing feels safer.

After a high NPS or satisfaction moment: Immediately following a positive service interaction or high survey score is prime territory for referral prompts.

In 2026, the savviest banks will move beyond “always-on” banners and instead orchestrate referral prompts around these behavioural triggers. When you ask at the right moment, you make it easy for satisfied customers to act.

Bank referral programme rules and compliance

Compliance matters in banking. Everyone knows that. The mistake many programmes make is letting legal language dominate the customer experience.

When rules feel dense or hidden in fine print, customers assume the reward will be hard to earn or harder to receive. That perception alone can stop them sharing. Clear rules reduce confusion. And confusion is friction.

Start with plain English. Spell out eligibility in one visible section, not three expandable tabs. If there are exclusions, say so upfront. If there are deadlines, make them obvious. Customers don’t mind rules, but often hate surprises.

A simple structure works best:

1. What your friend gets Be specific. “£75 when you open and fund your account with £500 within 30 days.”

2. What you get Mirror the clarity. “You’ll receive £75 once your friend qualifies.”

3. When it pays out Remove ambiguity. “Paid within 7 days of qualification.”

That three-part framing reduces perceived risk instantly. It answers the silent questions running through a customer’s head before they even ask them.

In finance, recommending a product feels personal. If customers aren’t fully confident in how the programme works, they won’t put their name behind it. Make the mechanics transparent, the timeline predictable, and the reward feel certain.

Clear compliance builds enough trust so that customers are comfortable saying, "you should try this", not just about satisfying regulators.

Tiered rewards and stacking (when usage is infrequent)

Banking products aren’t bought every week. That means you can’t rely on constant interaction to drive repeated referrals. If you want more than one share, you need to design for it.

Tiered rewards and stacking mechanics solve this.

There are two common approaches. The first is step-wise rewards. For example, £50 per successful referral. Clear. Predictable. Easy to understand.

The second is the classic “earn up to £500” model. This builds excitement and headline appeal, but it can feel distant if most customers only ever refer one friend. High ceilings don’t motivate if the first step feels flat.

The biggest issue? Most programmes see a sharp drop-off after the first referral, when customers share once, collect the reward, and stop. That second referral is where momentum dies.

So, incentivise it deliberately.

Instead of £50 per friend across the board, consider:

£40 for the first referral

£75 for the second

£100 for the third

Or unlock a higher-value perk once two friends qualify. The goal is to make referral number two feel like progress, not repetition.

When usage is infrequent, you won’t get endless chances to prompt customers. Tiered rewards create a reason to come back. And when structured properly, they turn a one-off action into a behaviour.

Measurement: KPIs for a bank referral programme

Bank referral programmes need performance metrics that go beyond “number of invites sent”. The goal is qualified, revenue-generating customers.

Here are the core KPIs that matter.

Share rate

The percentage of eligible customers who actually share a referral link. This tells you how compelling and visible your programme is. Low share rate usually means weak incentives, poor timing, or too much friction.

Qualified sign-up rate

The percentage of referred friends who complete the required qualifying action. Not just sign-ups. Funded accounts, approved applications, first spend. This is where quality starts to show.

Activation rate (funding / first use)

Of those who sign up, how many actually use the product? For banks, activation might mean funding an account, completing a first card transaction, making a transfer, or depositing into an investment account. This separates real customers from passive accounts.

CPA vs paid channels

Compare your cost per acquired, qualified customer through referral against paid search, social, and affiliates. Referral should compete on efficiency, not just volume.

Fraud rate

Track self-referrals, duplicate accounts, and reward abuse. A healthy programme has controls in place without damaging genuine participation.

Time to qualify

How long does it take for a referred friend to meet the qualifying criteria? Shorter times improve cash flow, customer satisfaction, and perceived reward certainty.

LTV and retention of referred users

Do referred customers stay longer? Hold more products? Generate higher customer lifetime value? In many financial services businesses, referral outperforms paid channels on long-term retention. That’s where the real upside sits.

Measure across the full funnel from share to long-term value. Because in banking, a referral programme must acquire the right customers and keep them.

A 90-day optimisation plan (what to test first)

If your referral programme isn’t delivering, don’t rip it out and start again. Optimise it in structured waves. Ninety days is enough time to generate meaningful learning without overwhelming your team or confusing customers.

Here’s a practical roadmap.

Weeks 1–2: Offer test

Start with the incentive. Test value and type. Cash vs points. £50 vs £75. Fee waiver vs boosted rate. Keep the mechanics stable so you can isolate the impact of the reward itself.

Also test double-sided vs single-sided rewards. When both the referrer and the friend benefit, share intent often increases.

In banking, that fairness dynamic matters. Customers are more comfortable recommending when they know their friend gains something tangible. Keep this phase clean and controlled. One variable at a time.

Weeks 3–6: Messaging test

Now refine how you position the programme. Test trust-led messaging alongside social capital angles. For example:

Security and reliability framing

“Smart move” positioning

Limited-time boost language

“Help a friend benefit” copy

Small wording changes can materially shift share rates, especially in financial services where perceived risk influences behaviour. Test subject lines, in-app prompts, landing page headlines, and share copy. Look for uplift in both share rate and qualified sign-ups.

Weeks 7–10: Placement and trigger test

Even the best incentive won’t perform if it’s buried. Test where and when you prompt referral:

In-app dashboard visibility

Post-activation prompts

After first card spend

Immediately following approval

At logout or account overview

Behavioural triggers often outperform static homepage banners. Customers are more receptive when they’ve just experienced value. Measure share rate by placement so you can see which moment truly drives action.

Weeks 11–12: Segmentation test

Once the fundamentals are stable, layer in segmentation. Test differentiated rewards for:

Premium vs mass-market customers

High-balance account holders

Recently activated users

High-intent cohorts who’ve just completed key actions

A uniform reward across your entire base rarely maximises performance. Premium customers may respond better to elevated perks or experiential benefits. Mass segments may prefer straightforward cash.

By the end of 90 days, you should have clear evidence on four levers: incentive, messaging, placement, and segment logic. That foundation gives you a referral programme that’s engineered, not assumed.

Conclusion

In 2026, a bank referral programme won’t stand out just because it exists. Most financial brands now have one. The real differentiator is how it’s designed.

The best programmes combine four things: trust, social value, low friction, and timing. Trust makes customers comfortable putting their name behind your brand. Social value gives them a reason to share beyond the reward. Low friction removes excuses. Timing catches customers at the moment their confidence is highest.

When those elements work together, referral stops being a bolt-on campaign and starts functioning as a reliable acquisition engine. One that brings in qualified, activated customers rather than low-intent sign-ups.

If you’re reviewing your current programme, start with the basics. Is the incentive distinctive? Are the rules clear? Are you prompting at the right moment? Are you measuring what actually matters?

And if you’re exploring how to test, segment, and optimise referral at scale, it may be worth seeing what a dedicated referral platform can unlock.

A short demo or audit of your current setup can quickly highlight missed opportunities. Sometimes the biggest gains come from refining what you already have.

Courtney Wylie

Courtney is VP of Product and Marketing for Mention Me. Helping leading eCommerce brands turbo charge their customer acquisition through fully flexible refer a friend programmes.

What Is a Referral Link? How to Create & Track One

What is a referral link, and how does it work? Learn how to create, share, and track referral links so you can attribute customer-led growth and optimise your referral programme.

.png)

.png)